Fed minutes, PCE inflation, Walmart earnings: 2/20/2023 - 2/24/2023

Earnings from Walmart and a key reading on inflation will offer investors the latest read on the health of the U.S. consumer in the holiday-shortened week ahead.

Markets

Dow Jones: 33,826.69 (+0.39%) 📈

S&P 500: 4,079.09 (-0.28%) 📉

Nasdaq: 11,787.27 (-0.58%) 📉

*Stock numbers as of market close on February 17th

Earnings from retail giants Walmart and Home Depot this week, along with the latest update on the Federal Reserve's preferred inflation measure and the minutes from the Fed's latest policy meeting, will be highlighted in the holiday-shortened week ahead.

U.S. stock and bond markets will be closed on Monday for President's day.

Results from Walmart and Home Depot, due out before the market opens on Tuesday, will offer further updates on the health of the U.S. consumer, which remains resilient in the face of stubbornly high inflation, most recently evidenced by January's retail sales data out last week.

")

On the economic data side, all eyes will be on the Personal Consumption Expenditures (PCE) price index — the Fed's most closely watched assessment of how quickly prices are rising across the economy — which is set for release Friday morning.

Prices in January likely jumped 0.5% over the prior month as measured by the PCE index, according to data from Bloomberg. in December, PCE inflation rose just 0.1% month-on-month. On an annual basis, PCE inflation is projected to come in at 5% in January, with no improvement from the year-over-year figure reported at the end of 2022.

Core PCE, which removes the volatile food and energy components out, is set to show a 0.4% climb over the prior month — ticking up slightly from 0.3% in December — and a marginally slower rise of 4.3% over the year, down from 4.4% in the last month of 2022.

If realized, those numbers would support recent indications inflation is not falling at the pace, and extent investors have been hoping for, even as prices have stabilized from the peaks of the current cycle.

The Consumer Price Index (CPI) out last week showed inflation picked up in January while cooling only slightly over the year to 6.4%. And producer prices shot up by the biggest amount in seven months in January.

This view has thwarted the market's recent momentum.

On Friday, the Dow Jones Industrial Average logged its third-straight losing week for the first time since September, closing down 0.1% for the five-day trading period.

The S&P 500 was down 0.3% for the week, its second consecutive week in the red, while the Nasdaq was an outlier, notching a weekly gain of 0.6%.

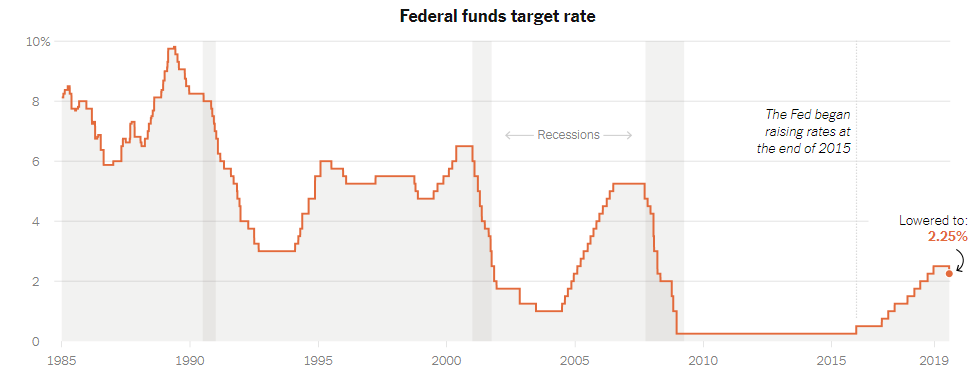

The bumpier-than-anticipated road to restoring price stability and strong economic data to start the year — nonfarm payrolls rose by 517,000 in January while retail sales surged 3% — have prompted Wall Street banks to revise their expectations for upcoming rate hikes by the Federal Reserve.

Teams at Goldman Sachs and Bank of America said this week they estimate three more rate increases this year; ahead of February's interest rate increase, some market participants had seen that move potentially marking the end of the Fed's rate hiking cycle.

Economists at Goldman Sachs and BofA each added additional 25-basis-point rate hikes in June to their forecasts, bringing both banks' projected estimates for the peak of the federal funds rate in this cycle to a new range of 5.25%-5.5%.

Bank of America also indicated strong evidence for a potential 0.50% increase at the Federal Reserve's next meeting in March.

"In our view, several forces would have to come together to cause the Fed to revert to a larger 50-basis-point rate hike," a team of strategists led by Michael Gapen said in a Friday note.

Minutes from the Federal Open Market Committee's (FOMC) meeting Jan. 31-Feb. 1 out Wednesday afternoon will offer insight into the thinking behind officials' 25-basis-point increase earlier in the month.

Cleveland Fed President Loretta Mester said in a speech Thursday she would have favored raising interest rates by 0.50%, asserting that she and her colleagues have further work to do in taming inflation.

"The FOMC has come an appreciable way in bringing policy from a very accommodative stance to a restrictive one, but I believe we have more work to do," Mester said at a Global Interdependence Center conference at the University of South Florida Sarasota-Manatee College of Business.

"I don’t want to surprise the markets," Mester said. "We're better if we explain. In that meeting there was an economic case for [a 50 basis point increase] in my view, but the market wasn't expecting that. That does factor into my views about the proper thing to do at a meeting."

On the earnings side, Walmart will kick off a busy week of quarterly reports from Corporate America on Tuesday.

CFRA Research senior equity analyst Arun Sundaram predicts the supermarket giant will see continued trade-down benefits from inflation, particularly from higher-income customers, which is expected to boost its membership program Walmart+.

Macroeconomic uncertainty, however, does pose some downside risks to the company. Among those potential headwinds are weaker consumer spending from lower-income consumers, given elevated inflation and rising interest rates, bigger markdowns on inventories, and continued product, wage, and transportation cost pressures.

Other notable earnings results in the upcoming week will come from Home Depot, Alibaba, Keurig Dr. Pepper, Live Nation, Moderna, PG&E, and Warner Bros. Discovery, among others.

Beaten-up names like Coinbase and Carvana will also report numbers after a junk rally that has lifted shares this year.

Events Calendar

Monday, February 20

Markets closed for President's Day. No notable reports are scheduled for release.

Tuesday, February 21

Philadelphia Fed Non-Manufacturing Activity Index, February (-6.5% during the prior month)

S&P Global U.S. Manufacturing PMI, February Preliminary (47.2 expected, 46.9 during prior month)

S&P Global U.S. Services PMI, February Preliminary (47.3 expected, 46.8 during the prior month)

S&P Global U.S. Composite PMI, February Preliminary (47.5 expected, 46.8 during prior month)

Existing Home Sales, January (4.10 million expected, 4.02 million during prior month)

Existing Home Sales, month-over-month, January (-2.0% expected, -1.5% during prior month)

Coinbase Global COIN 0.00%↑, Cracker Barrel CBRL 0.00%↑, Home Depot HD 0.00%↑, Hostess Brands TWNK 0.00%↑, La-Z-Boy LZB 0.00%↑, Palo Alto Networks PANW 0.00%↑, Tanger Factory Outlet Centers SKT 0.00%↑, Toll Brothers TOL 0.00%↑, Walmart WMT 0.00%↑, ZipRecruiter ZIP 0.00%↑

Wednesday, February 22

MBA Mortgage Applications, Feb. 1, the week ended Feb. 17 (-7.7% during the prior week)

FOMC Meeting Minutes, Feb. 1

Allbirds BIRD 0.00%↑, Altice USA ATUS 0.00%↑, Baidu BIDU 0.00%↑, Bath & Body Works BBWI 0.00%↑, Bumble BMBL 0.00%↑, Cheesecake Factory CAKE 0.00%↑, eBay EBAY 0.00%↑, Etsy ETSY 0.00%↑, Fidelity National FNF 0.00%↑, Lemonade LMND 0.00%↑, Lucid Group LCID 0.00%↑, Marriott Vacations VAC 0.00%↑, Overstock.com OSTK 0.00%↑, Rent-A-Center RCII 0.00%↑, Teladoc TDOC 0.00%↑, TJX TJX 0.00%↑, United Therapeutics UTHR 0.00%↑, Wingstop WING 0.00%↑, Wolverine World Wide WWW 0.00%↑

Thursday, February 23

Chicago Fed National Activity Index, September (-0.49 during the prior month)

GDP Annualized, quarter-over-quarter, 4Q Second Estimate (2.9% expected, 2.9% prior)

Personal Consumption, quarter-over-quarter, 4Q Second Estimate (2.0% expected, 2.1% prior)

GDP Price Index, quarter-over-quarter, 4Q Second Estimate (3.5% expected, 3.5% prior)

Core PCE, quarter-over-quarter, 4Q Second Estimate (3.9% expected, 3.9% prior)

Initial Jobless Claims, the week ended Feb. 18 (220,000 expected, 194,000 during the prior week)

Continuing Claims, the week ended Feb. 11 (1.696 million during the prior week)

Kansas City Fed Manufacturing Activity, February (-2 expected, -1 during the prior month)

Alibaba Group Holding BABA 0.00%↑, Autodesk ADSK 0.00%↑, Beyond Meat BYND 0.00%↑, Block SQ 0.00%↑, Booking Holdings BKNG 0.00%↑, Cars.com CARS 0.00%↑, Carvana CVNA 0.00%↑, CubeSmart CUBE 0.00%↑, Dillard's DDS 0.00%↑, DISH Network DISH 0.00%↑, Domino's Pizza DPZ 0.00%↑, Farfetch FTCH 0.00%↑, Intuit INTU 0.00%↑, Keurig Dr. Pepper KDP 0.00%↑, Live Nation LYV 0.00%↑, Moderna MRNA 0.00%↑, Nikola NKLA 0.00%↑, Papa John's PZZA 0.00%↑, PG&E PCG 0.00%↑, Planet Fitness PLNT 0.00%↑, Steven Madden SHOO 0.00%↑, Warner Bros. Discovery WBD 0.00%↑, Wayfair W 0.00%↑, YETI Holdings YETI 0.00%↑

Friday, February 24

Personal Income, month-over-month, January (0.9% expected, 0.2% during prior month)

Personal Spending, month-over-month, January (1.3% expected, -0.2% during prior month)

Real Personal Spending, month-over-month, January (1.1% expected, -0.3% during prior month)

PCE Deflator, month-over-month, January (0.5% expected, 0.1% during the prior month)

PCE Deflator, year-over-year, January (5.0% expected, 5.0% during prior month)

PCE Core Deflator, month-over-month, January (0.4% expected, 0.3% during the prior month)

PCE Core Deflator, year-over-year, January (4.3% expected, 4.4% during the prior month)

New Home Sales, January (620,000 expected, 616,000 during prior month)

New Home Sales, month-over-month, January (0.7% expected, 2.3% during prior month)

The University of Michigan Consumer Sentiment, February Final (66.4 expected, 66.4 prior)

Kansas City Fed Services Activity, February (-11 during the prior month)

Carter's CRI 0.00%↑, E.W. Scripps SSP 0.00%↑

If you have found this article helpful, I would really appreciate it if you clicked the like button and shared this post. Thank you so much for reading! Have a wonderful week :)

Looks like Biden is moving us to Jimmy Carter rates if this keeps up. You are welcome.

thank you